Economic growth is forecast to remain low in Mongolia this year before picking up in 2023, according to the Asian Development Bank (ADB). Meanwhile, inflation and the current account deficit are expected to outpace earlier projections.

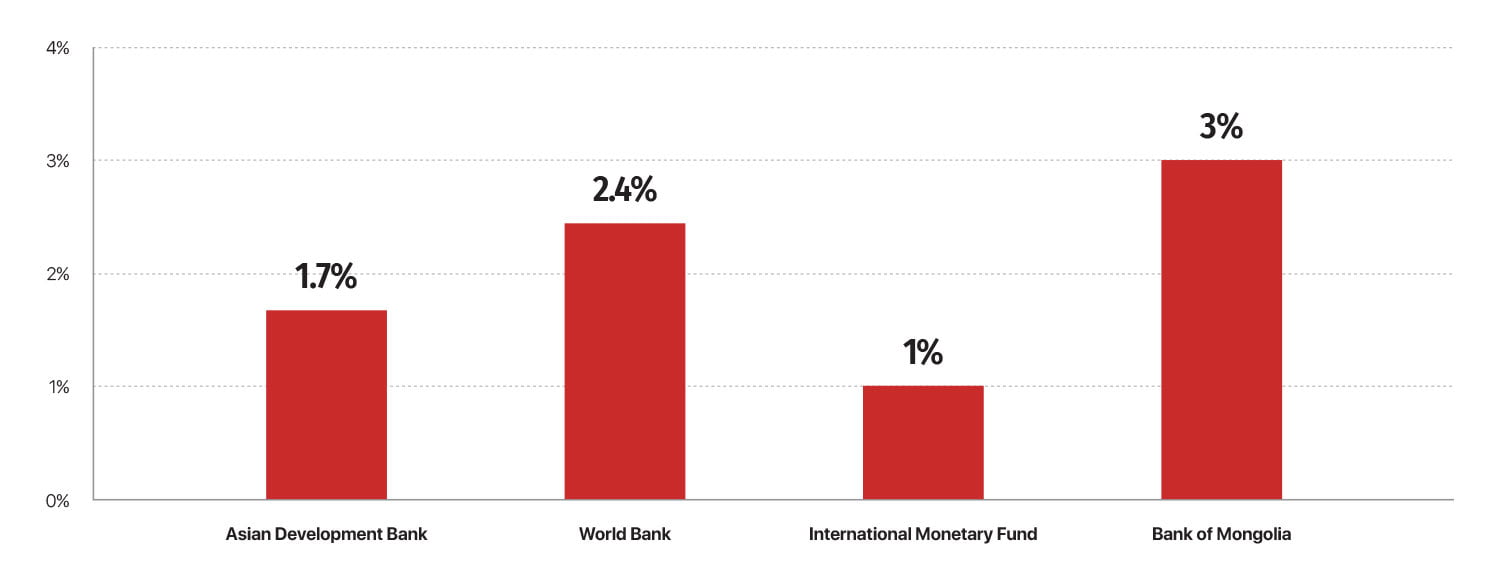

Growth is forecasted at 1.7% this year, down from an April projection of 2.3%. The forecast for next year is also cut to 4.9% from 5.6%. This is due to prolonged border restrictions, deterioration of purchasing power under persistently high inflation, higher borrowing costs, a likely decline in the availability of credit, and a continuation of monetary tightening.

Mongolia's economic growth projections, 2022

“Despite initial signs of recovery, the economy’s near-term growth prospects remain uneven,” said ADB Country Director for Mongolia Pavit Ramachandran. “A combination of persistently high inflation and a large current account deficit creates a pressing need for achieving better macroeconomic balance while focusing on medium-term structural reforms.”

The prolonged restrictions at the border with the PRC as well as the Russian invasion of Ukraine have disrupted trade, reduced essential imports, increased import prices, escalated price increases, and dampened industrial sectors and business sentiment. Contraction continued in the mining, manufacturing, construction, and transportation sectors, and recovery in industry is likely to take time. Still, the lifting of pandemic-related restrictions since February 2022 has revived domestic demand, assisted by accommodative monetary and fiscal policies.

Inflation escalated and remained above the central bank’s target for the past 16 consecutive months. The surge in inflation will continue, mainly due to persistent supply disruptions, rising transportation costs, exchange rate depreciation and its pass-through impacts, and higher prices for food, fuel, and imported durables.

Downside risks to the outlook are any new restrictions at major trade portals with the PRC, a decline in mineral commodity prices, negative spillovers from the global slowdown, aggressive monetary tightening, or rising balance sheet risks in the domestic financial sector.